Introduction

When searching for a pnb personal loan, borrowers are typically looking to understand the unsecured credit facility offered by Punjab National Bank (PNB). In simple terms, this keyword represents a multi-purpose loan that does not require collateral, allowing individuals to meet urgent financial needs such as medical emergencies, wedding expenses, or home renovation. Borrowers search for this specific product to evaluate its affordability, primarily focusing on the interest rates and repayment flexibility. The final cost of a pnb personal loan is heavily affected by the Repo Linked Lending Rate (RLLR), the borrower’s employer category (government vs. private), and their individual credit score (CIBIL).

At loanrejectionhelp.com, our mission is to empower you with financial literacy. Before you worry about the application process or the stress of a potential loan rejection, it is vital to understand how this financial instrument works. Knowing the mechanics of interest calculation and the impact of market rates will help you decide if this is the right responsible borrowing path for you.

Table of Contents

What is a PNB Personal Loan? (The Concept of Unsecured Credit)

A PNB personal loan is an “unsecured” lending product. Unlike a home loan or a car loan, where the asset acts as security, a personal loan is granted based on your “promise to pay.” PNB evaluates your income stability and past credit behavior rather than asking for a physical asset as a guarantee.

Because there is no collateral, the bank takes on a higher risk. To balance this risk, the interest rates are generally higher than those for secured loans but lower than credit card interest rates. This makes it a popular tool for debt consolidation or high-value personal spending.

How Interest Rates Work: The RLLR Mechanism

One of the most critical aspects of a pnb personal loan is how the interest rate is determined. As of 2026, PNB primarily follows the Repo Linked Lending Rate (RLLR) framework for its retail advances.

1. The Benchmark (Repo Rate)

The Repo Rate is the rate at which the Reserve Bank of India (RBI) lends money to commercial banks. When the RBI changes this rate to control inflation, PNB’s RLLR—and consequently your loan’s interest rate—moves in tandem. This means if you have a floating-rate loan, your EMIs might increase or decrease based on national economic policy.

2. The Mark-up (Spread)

PNB adds a “mark-up” or “spread” over the RLLR. This spread is determined by:

- Borrower Category: Government employees and defense personnel (often under schemes like PNB Rakshak Plus) often enjoy lower spreads compared to private-sector employees.

- Relationship with the Bank: Existing PNB account holders, particularly those with salary accounts, may receive preferential rates.

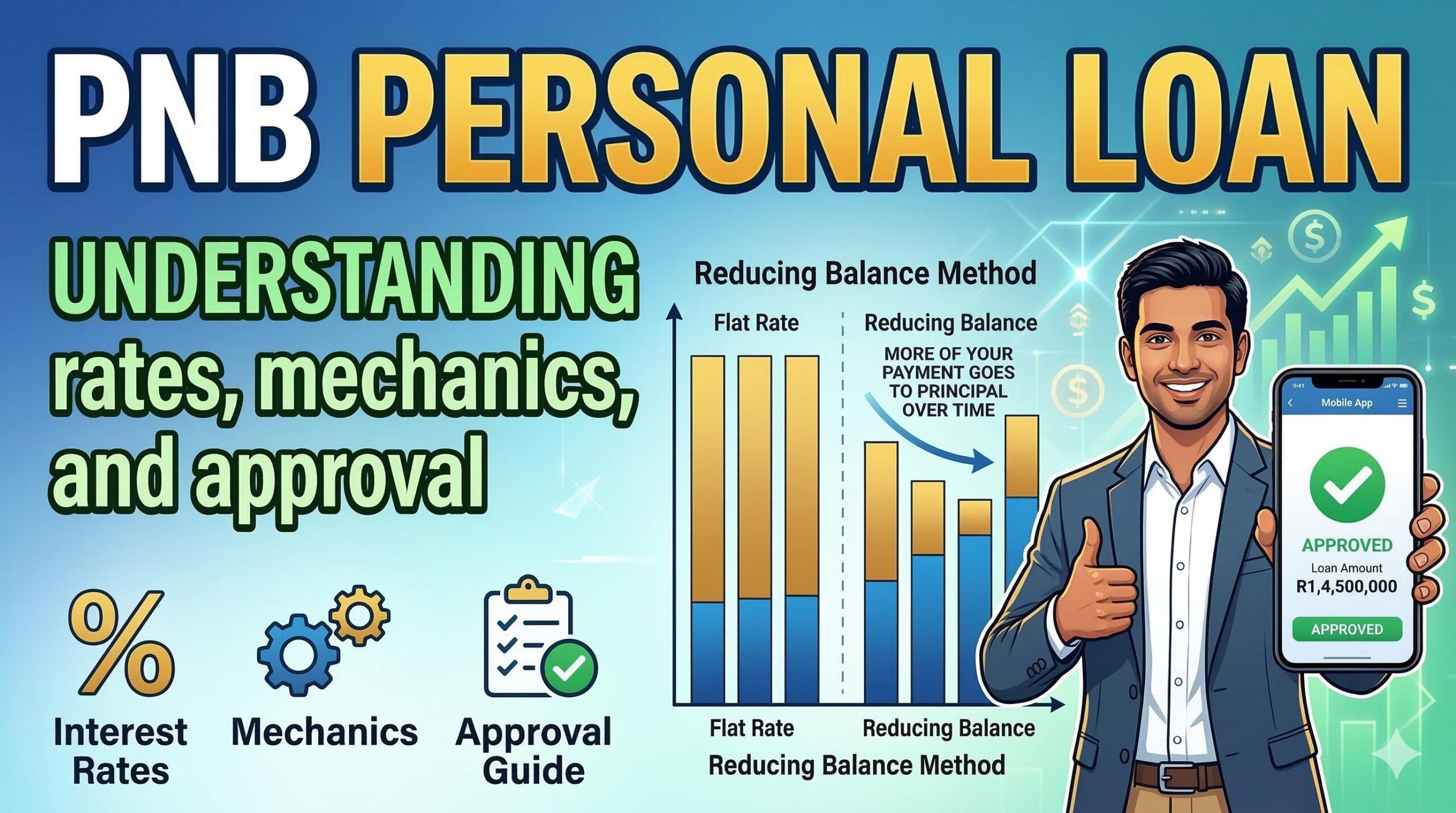

3. Reducing Balance Method

PNB usually calculates interest using the Daily Reducing Balance method. Unlike a “flat rate” where interest is charged on the original loan amount for the entire tenure, the reducing balance method calculates interest only on the outstanding principal. As you pay your monthly installments, the interest component decreases, and the principal repayment component increases.

Key Factors That Determine Your Loan Cost

Beyond the market benchmark, several personal variables dictate the final “interest burden” of your pnb personal loan.

Credit Score (CIBIL)

Your CIBIL score is a numerical summary of your credit history. A score of 750 or above signals to PNB that you are a low-risk borrower. High-score applicants are often rewarded with the “best available” interest rates, whereas lower scores might attract a “risk premium” (higher interest) or lead to outright rejection.

Loan Tenure and EMI

PNB offers flexible tenures, often up to 60 or 72 months. While a longer tenure reduces your monthly EMI, it significantly increases the total interest paid over the life of the loan. Conversely, a shorter tenure means higher EMIs but a cheaper loan overall.

Understanding Loan Rejection and Approval for PNB

At loanrejectionhelp.com, we know that a rejection can be a major setback. However, understanding why PNB might decline an application allows you to fix your financial profile before applying.

Why Applications Get Rejected

- High FOIR (Fixed Obligation to Income Ratio): Banks calculate how much of your monthly salary is already going toward existing debts (rent, other loans, credit cards). If your total obligations exceed 50–60% of your income, PNB may reject your application to prevent over-indebtedness.

- Low Credit Score: If your report shows late payments, defaults, or “written-off” accounts, PNB views you as a high-risk applicant.

- Employment Type: PNB has specific preferences for permanent employees of Central/State Govt, PSUs, and reputed corporate institutions. Self-employed individuals may face stricter criteria, such as a minimum annual income and at least two years of business stability.

Strategies to Improve Approval Odds

- Check Your Credit Report: Ensure there are no errors in your CIBIL report at least three months before applying.

- Consolidate Small Debts: Close small credit card balances to lower your FOIR.

- Opt for a Salary Account: If possible, move your salary account to PNB. “Check-off” facilities (where EMIs are deducted directly from salary) significantly boost approval chances.

- Stability Matters: Avoid applying immediately after changing jobs. Lenders prefer at least 1–2 years of continuous service.

HDFC Bank Personal Loan Interest Rate: A Complete Guide to Rates and Approvals

Frequently Asked Questions (FAQ)

1. Is the interest rate on a PNB personal loan fixed or floating?

PNB typically offers floating rates linked to the RLLR. This means your rate can change during the tenure if the RBI adjusts the Repo Rate. However, some special schemes or fixed-period options might exist—always verify the latest “Sanction Letter” for your specific terms.

2. Are there any hidden charges?

While the interest rate is the primary cost, you should also account for Processing Fees (usually up to 1% of the loan amount), Documentation Charges, and Stamp Duty. PNB is known for transparency, often waiving prepayment penalties if the loan is closed from your own identifiable sources.

3. Can pensioners apply for a PNB personal loan?

Yes, PNB has specialized schemes for pensioners (e.g., Personal Loan Scheme for Pensioners). These often feature lower interest rates and allow repayment up to the age of 78, provided the pension is drawn through a PNB branch.

Conclusion: Borrowing Responsibly

A pnb personal loan is a versatile financial tool, but it should be used with discipline. By understanding that your interest rate is a combination of national policy (Repo Rate) and your personal credit behavior (CIBIL), you can take control of the cost of your credit.

Remember, a loan is a liability that must be serviced from your future income. At loanrejectionhelp.com, we recommend a “needs-only” approach to personal credit. Maintain a healthy credit score, keep your debt-to-income ratio low, and always read the fine print regarding the Daily Reducing Balance method to ensure you are getting the most cost-effective deal.

Educational Disclaimer: The information provided in this article is for educational purposes only and does not constitute financial advice. Interest rates, eligibility criteria, and bank policies are subject to change at the discretion of Punjab National Bank. Always verify the latest terms on the official PNB website or visit a branch before applying.

1 thought on “Understanding the PNB Personal Loan: Interest Rates, Mechanics, and Approval Guide”