Educational Disclaimer: The information provided on LoanRejectionHelp.com is for educational and informational purposes only. It does not constitute professional financial advice. All loan approvals are subject to the individual lender’s terms, conditions, and internal policies. Always practice responsible borrowing.

Introduction

Have you ever applied for a personal loan with a fantastic credit score and a solid salary, only to face an unexpected employer category loan rejection? This specific type of credit denial occurs when a bank or financial institution rejects your loan application because your employer is classified as high-risk, unlisted, or falls into an unfavorable tier within the lender’s internal grading system. Borrowers actively search for this term because they are often left confused and frustrated when their personal financial habits are excellent, yet they are denied credit purely based on where they work.

Ultimately, this specific rejection is affected by your company’s overall size, financial stability, industry reputation, and whether the lender has an existing corporate relationship with your workplace.

Understanding how lenders evaluate your employer is a crucial part of financial literacy. While you can control your credit score, knowing how the banking system views your job can help you navigate the borrowing process much more effectively.

Table of Contents

What is Employer Categorization in Banking?

To understand an employer category loan rejection, you first need to understand the financial concept of “Employer Categorization.”

When you apply for an unsecured loan (like a personal loan or credit card), lenders take on a significant amount of risk since there is no collateral backing the debt. To manage this risk, lenders evaluate not just your past credit history, but your future ability to repay. This relies heavily on your job stability.

Banks maintain massive internal databases where they grade and categorize thousands of companies. While every bank has its own specific system, they generally divide employers into the following tiers:

to unlisted companies (Red_C).")

- Category A (Super A / Target): Top multinational corporations (MNCs), large publicly traded companies, Fortune 500 firms, and government departments. These are viewed as ultra-stable. Employees here rarely face job volatility, so lenders offer them the highest approval odds and the lowest interest rates.

- Category B: Well-established mid-sized companies and regional leaders. They are considered safe, but borrowers might receive slightly lower loan amounts or standard interest rates compared to Category A.

- Category C: Smaller private limited companies, newer businesses, or industries prone to economic fluctuations. Lenders view these as higher risk.

- Unlisted / Delisted Companies: Startups, very small local businesses, or companies that have not yet been evaluated by the bank’s risk department. If your company is here, the chances of an employer category loan rejection are highly elevated.

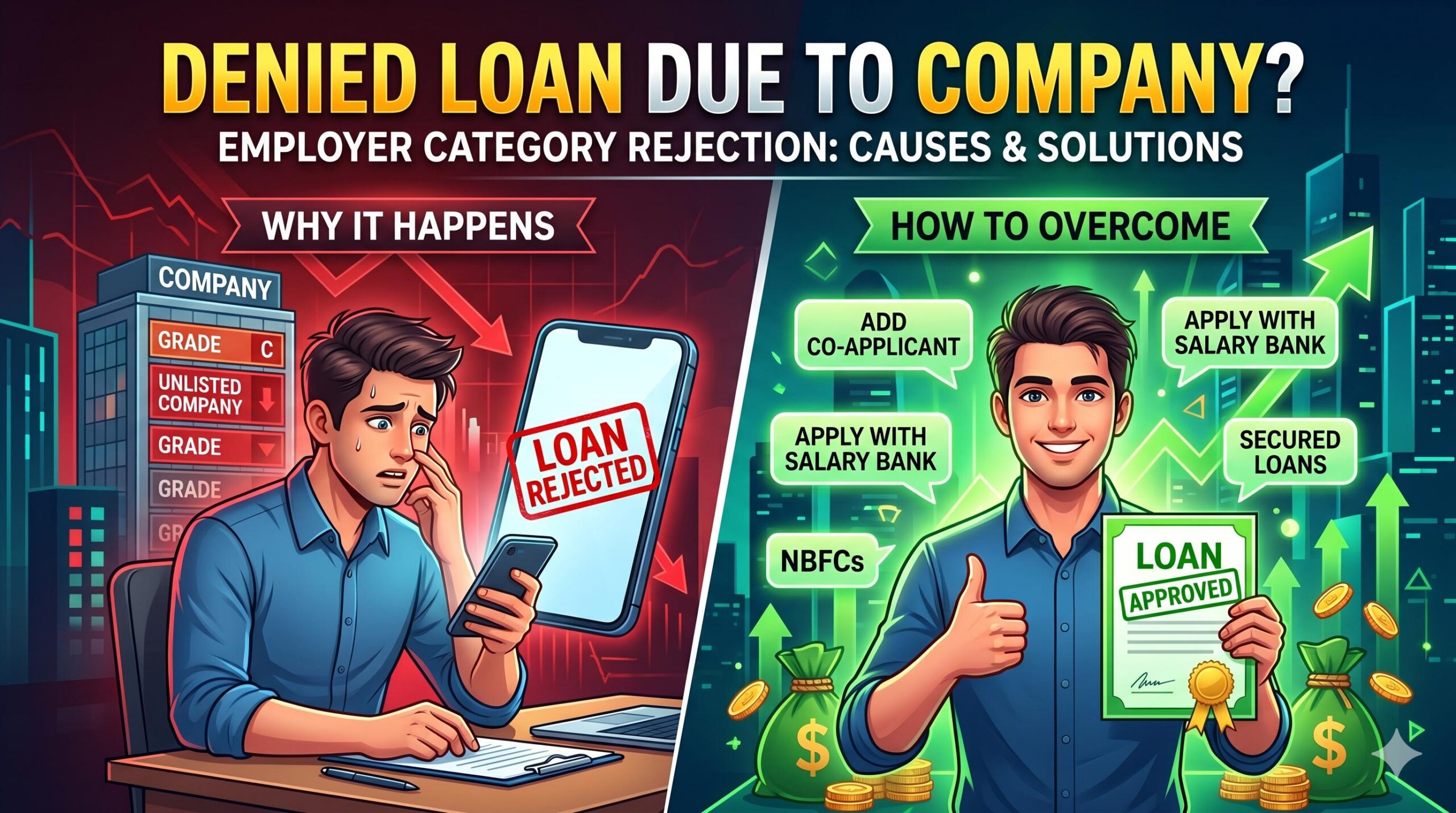

Why Does an Employer Category Loan Rejection Happen?

Lenders are highly analytical. If your loan application is denied due to your employer’s category, it usually boils down to the lender’s automated risk assessment models. Here is why the rejection occurs:

1. Perceived Income Instability

Banks rely on the assumption that you will receive a steady paycheck for the entire tenure of the loan (which could be up to 5 years). If your employer is in Category C or unlisted, the bank’s risk model assumes a higher statistical probability of company layoffs, delayed salaries, or business closure.

2. High Industry Attrition Rates

Certain sectors—like early-stage tech startups, seasonal tourism, or commission-heavy sales agencies—have notoriously high employee turnover. Even if your company is legitimate, the broader industry risk can negatively impact your employer’s categorization.

3. Lack of Corporate Verification

If your employer is unlisted, it simply means the bank has no financial data on them. Lenders cannot easily verify the company’s profit margins, vintage (years in business), or compliance records. Rather than spending time investigating a small, unknown company, automated banking systems will often issue a default rejection to play it safe.

How to Overcome This Type of Loan Rejection

An employer category loan rejection can be disheartening, but it is not the end of your financial journey. If you find yourself in this situation, here are responsible, educational steps you can take to improve your credit profile and approval odds:

Apply with Your Salary Account Bank

If your company is unlisted or poorly categorized, your best chance of approval is with the bank where your salary is deposited every month. This bank has internal data proving that your salary credits are consistent, on-time, and stable, which can sometimes override a poor employer category.

Add a Strong Co-Applicant

If your spouse, parent, or sibling works for a Category A or B employer, consider applying for the loan jointly. The primary lender will take the co-applicant’s stable employer profile into account, significantly lowering the overall risk of the application.

Explore Non-Banking Financial Companies (NBFCs)

Traditional, top-tier banks have the strictest employer category rules. NBFCs and digital lending platforms often use alternative credit scoring models. While they might charge slightly higher interest rates to offset the risk, they are generally much more accommodating to employees of startups and unlisted companies.

Consider Secured Borrowing

If you urgently need funds and unsecured routes are blocked, consider loans backed by collateral. Options include a loan against a fixed deposit, a gold loan, or borrowing against mutual funds. Because these are secured, the lender rarely considers your employer’s category.

Responsible Borrowing & Risk Awareness

Whenever you face a loan rejection of any kind, do not immediately apply to multiple other banks. Every time you apply for credit, a “hard inquiry” is placed on your credit report. Multiple inquiries in a short period will drastically lower your credit score and make you look desperate for funds, leading to further rejections. Instead, take a pause, investigate the specific reason for the denial, and strategically choose your next step.

Understanding the Kredito24 Loan: Features, Eligibility, and Why Applications Get Rejected

Frequently Asked Questions (FAQ)

Q: Can I get an employer category loan rejection even with a 750+ credit score?

A: Yes. A credit score reflects your past repayment behavior, but the employer category reflects your future income stability. Banks require both to be strong for unsecured loan approvals.

Q: How can I check my company’s category?

A: Employer categorization is strictly internal to each bank and is not public information. However, you can usually gauge it by asking your HR department if they have formal corporate tie-ups with any specific banks for salary accounts.

Q: Will my company ever move to a better category?

A: Yes. As your company grows in revenue, employee size, and years in business, its financial footprint expands. Over time, banks frequently update their databases and may upgrade your employer to Category B or A.