Introduction

When planning for a financial emergency, a major expense, or debt consolidation, the HDFC Bank personal loan interest rate is one of the most critical figures borrowers search for. This rate represents the exact cost of borrowing unsecured funds from the bank. Borrowers actively seek out this information because it directly determines their Equated Monthly Installment (EMI) and the total financial burden of the loan over its tenure. However, this rate is not a single, universal number. What affects the final interest rate you are offered includes your credit history (CIBIL score), employment stability, employer categorization, and your existing debt-to-income ratio. Understanding how this specific rate is calculated is the ultimate key to securing affordable credit and avoiding application rejection.

Educational Disclaimer: This article is strictly for educational and informational purposes. The interest rates, eligibility criteria, and banking policies discussed are based on general industry practices and historical data. We do not guarantee loan approvals or specific interest rates. Always consult directly with HDFC Bank or a certified financial advisor before making borrowing decisions. Borrowing involves financial risk.

Table of Contents

What is the HDFC Bank Personal Loan Interest Rate?

To make informed borrowing decisions, you must first understand what an interest rate actually represents. In the context of a personal loan, the interest rate is the percentage of the principal loan amount that the bank charges you for the privilege of borrowing their money.

Because personal loans are “unsecured”—meaning you do not have to pledge assets like gold, property, or a vehicle as collateral—the bank takes on a significantly higher level of risk. If a borrower defaults, the bank has no physical asset to seize to recover its funds. To compensate for this heightened risk, personal loan interest rates are naturally higher than those of secured loans.

When you look up the HDFC Bank personal loan interest rate, you will usually see a “range” (for example, starting from 10.50% to upwards of 21.00% per annum). The bank uses a sophisticated risk-based pricing model. This means the lowest advertised rates are reserved strictly for applicants who pose the absolute lowest risk of default. If your financial profile shows slight inconsistencies or higher risk, the bank may still approve your loan, but they will offset their risk by charging you a higher interest rate near the top of that range.

Key Factors That Determine Your Specific Interest Rate

Lenders do not assign interest rates randomly. When you submit an application, the bank’s underwriting algorithms meticulously analyze your financial profile to determine exactly where you fall within their interest rate range. Here are the primary factors that dictate your rate:

1. Your Credit Score (CIBIL Score)

Your credit score is the single most influential factor in determining your personal loan interest rate. In India, a CIBIL score ranges from 300 to 900.

- High Scores (750 – 900): Applicants in this tier have a proven track record of repaying credit cards and past loans on time. Because they are low-risk, they are offered the lowest possible interest rates.

- Average Scores (650 – 749): These applicants might have a few late payments or high credit utilization. They may be approved, but at a moderately higher interest rate.

- Low Scores (Below 650): A low score usually leads to outright application rejection. The perceived risk of default is too high for the bank to justify lending, regardless of the interest rate they could charge.

2. Employer Category and Company Profile

Banks categorize employers into different tiers (often labeled as Super A, A, B, and C lists). If you work for a top-tier multinational corporation, a prominent public sector enterprise, or a highly reputed blue-chip company, banks view your job—and therefore your income—as highly stable. Employees of these categorized companies are frequently offered preferential, lower interest rates. Conversely, if you work for an unlisted startup or a very small proprietorship, the bank perceives a higher risk of job instability, resulting in a higher interest rate.

3. Net Monthly Income

While your income determines the amount of the loan you qualify for, it also subtly influences your rate. Higher-income earners generally have more disposable income to absorb financial shocks, making them safer borrowers. Therefore, an individual earning ₹1,00,000 per month might negotiate a slightly better interest rate than someone earning the minimum required threshold of ₹25,000 per month, assuming all other factors are equal.

4. Existing Banking Relationship

If you already have a salary account, a long-standing savings account, or a good track record with an existing credit card at HDFC Bank, you are a known entity. Banks are often willing to offer a discounted interest rate to their existing, loyal customers compared to completely new walk-in applicants.

How Interest Rates Intersect with Loan Rejection

over the limit and leading to loan rejection.")

Many borrowers misunderstand the relationship between interest rates and loan rejection. They assume that if they have a slightly poor financial profile, the bank will just charge them a massive interest rate. However, responsible lending policies prevent this. Here is how the interest rate directly impacts your approval or rejection:

The Fixed Obligation to Income Ratio (FOIR)

Banks use a metric called FOIR (or Debt-to-Income ratio) to ensure you are not over-borrowing. As a rule of thumb, lenders do not want your total monthly debt payments (including the new loan’s EMI) to exceed 40% to 50% of your net take-home salary.

Here is where the HDFC Bank personal loan interest rate becomes the deciding factor:

- The bank evaluates your profile and assigns you an interest rate based on your risk.

- They calculate what your new EMI will be at that specific interest rate.

- If your profile is risky, your assigned interest rate is high. A high interest rate creates a larger monthly EMI.

- If this large EMI pushes your total monthly debt obligations over the 50% FOIR limit, the loan is rejected.

In short, a poor financial profile doesn’t just result in a high interest rate; it creates a mathematical reality where the required EMI becomes unaffordable according to bank regulations, leading directly to application rejection.

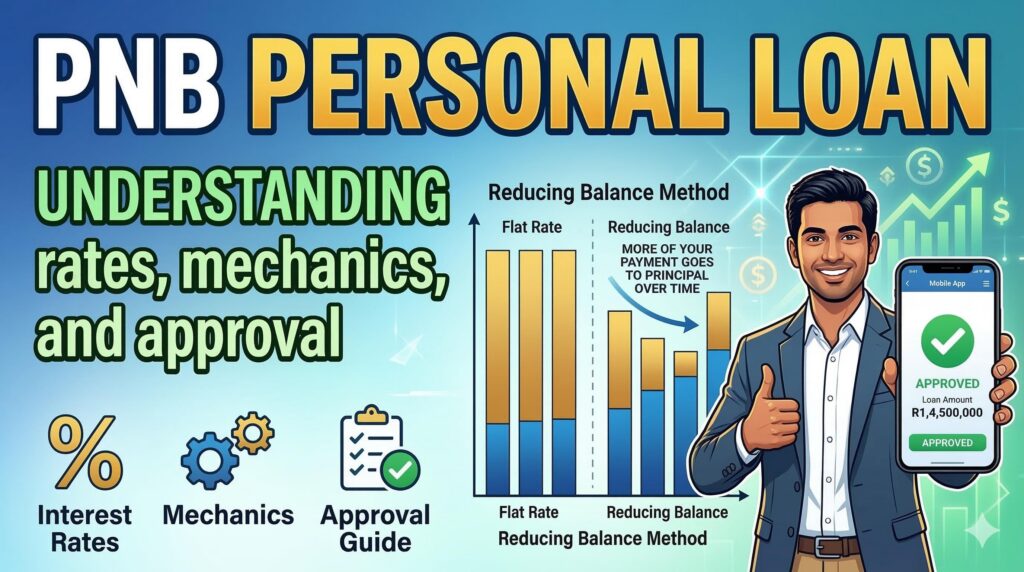

Understanding the Calculation: Reducing Balance Method

It is vital to understand how the interest is applied to your loan. Most major financial institutions, including HDFC Bank, calculate personal loan interest on a Reducing Balance (or Diminishing Balance) method, rather than a Flat Rate method.

- Flat Rate: Interest is calculated on the entire original principal amount for the whole tenure of the loan, regardless of how much you have already paid back. This is generally more expensive.

- Reducing Balance Rate: The interest for each month is calculated only on the outstanding principal balance. As you pay your EMI each month, a portion goes toward the principal. The next month, the interest is calculated on that new, slightly smaller principal amount.

This means that a 15% reducing balance interest rate is vastly cheaper than a 15% flat interest rate. Always ensure you understand which calculation method a lender is using before signing an agreement.

Step-by-Step Ways to Secure the Best Rate and Avoid Rejection

Securing a favorable interest rate is entirely dependent on presenting a low-risk profile to the lender. Here are practical, actionable steps to improve your standing:

Step 1: Check and Correct Your Credit Report

Before applying and subjecting yourself to a hard credit inquiry, download your credit report from a major bureau. Check for any administrative errors, such as loans you have already closed that are still showing as active. Disputing and fixing these errors can instantly improve your score, qualifying you for a lower interest rate tier.

Step 2: Pay Down Existing Revolving Debt

If your credit cards are maxed out, your credit utilization ratio is high. Lenders view this as credit-hungry behavior. Pay down your credit card balances so your utilization is below 30% of your total limit. This action dramatically improves your CIBIL score and lowers your FOIR, paving the way for a better interest rate.

Step 3: Consolidate Applications

Do not apply to five different banks simultaneously hoping to compare rates. Every application triggers a “hard inquiry” on your credit report, which temporarily lowers your score. Multiple inquiries signal financial desperation and can cause a bank to increase your interest rate or reject the application outright.

Step 4: Choose the Right Tenure

While selecting a longer loan tenure (e.g., 5 years instead of 3 years) reduces your monthly EMI, it vastly increases the total amount of interest you will pay to the bank over the life of the loan. Furthermore, banks sometimes offer slightly lower interest rates for shorter tenures because their funds are tied up for less time. Balance your need for an affordable EMI with the goal of paying as little total interest as possible.

Navigating Rejections: Your Guide to the Bajaj Finserv Personal Loan

Responsible Borrowing: Assessing Your True Cost

Understanding the HDFC Bank personal loan interest rate is fundamentally about understanding the true cost of your borrowing. An interest rate is not just an abstract percentage; it is real money leaving your pocket every month.

Before you apply, practice responsible borrowing:

- Use an EMI Calculator: Always use an online calculator to see exactly how different interest rates affect your monthly cash flow.

- Look Beyond the Rate: Remember to account for processing fees, documentation charges, and pre-payment penalties. A loan with a slightly lower interest rate but massive processing fees might actually be more expensive in the long run.

- Borrow Only What You Need: Do not let a bank up-sell you. If you need ₹3,00,000 to cover a medical emergency, do not take ₹5,00,000 just because you are eligible. You will be paying interest on that extra ₹2,00,000 for years.

Conclusion

The HDFC Bank personal loan interest rate is the central pivot around which your entire borrowing experience revolves. It dictates your monthly affordability, your total financial liability, and heavily influences whether your application will be approved or rejected by the bank’s strict risk-assessment algorithms.

By taking the time to understand how this rate is determined—through your credit score, employer stability, and debt-to-income ratio—you transition from a passive applicant hoping for approval into an informed consumer who can actively negotiate better terms.

Take charge of your financial health. Monitor your credit report, keep your existing debts low, and approach borrowing with a clear, well-calculated repayment plan.

Would you like to explore more comprehensive guides on how to rebuild a damaged credit score before you apply for your next loan?

1 thought on “HDFC Bank Personal Loan Interest Rate: A Complete Guide to Rates and Approvals”